Two years of COVID reset tea consumption at restaurants and cafés, initially reinforcing traditional expectations of comfort and warmth but evolving to permanently disrupt delivery, takeaway, menu choices, and celebratory occasions with tea. Tea (except for bubble tea) largely missed out on the rapid growth of restaurant-quality food delivery, curbside service, and take-out. Beverage service in downtown offices, sales at transit terminals, and inner-city stands remain below pre-pandemic levels. Retail vendors offering afternoon tea at tourist locations, iced tea at sports venues, and food trucks selling teas and juice lost sales to homebound tea drinkers purchasing online or near-to-home suburban locations. COVID reversed the sales growth of tea as a breakfast alternative. Independently operated tearooms with few seats and limited financial resources closed, changed owners, or pivoted online. Tea is consumed more frequently at home, and with food inflation rising and costs driving up menu prices, it is clear that in 2022 tea retail will not return to the familiar patterns of yesteryear.

- Caption: Reinventing tea retail, a TEAIN22 Foodservice Forecast

Hear the forecast

Reinventing Tea Retail

By Dan Bolton

The pandemic continues to exert a heavy hand. Everything is so unpredictable that the best advice for a battered tea segment is to stand pat. If 24 months of turmoil has not bankrupted your venture, now is not the time to exit. Those who qualify should judiciously spend government assistance and wait.

Above all, don’t sell out because of Omicron. Retail sales of tea are stubbornly reliable during periods of crisis. Demand for conventional black tea may be flat in developed countries, but tea consumption has more than doubled to 6.4 billion kilos since 2000 — per capita consumption held at 400 grams per capita. According to the Tea Association of the USA, the US tea market grew in 2021 and is now valued at more than $13 billion.

“Tea in the United States was uniquely vulnerable to Coronavirus (COVID-19) since an unusually high proportion of it is consumed at foodservice,” writes Euromonitor beverage analyst Matthew Barry. In 2019, that proportion was 48%. Statista estimates that 52% of spending and 5% of volume consumption in the tea segment will be out-of-home by 2025.

TEAIN22 Forecast: The upheaval in foodservice is manageable. Fears that keep diners away from cafés are diminishing. Out-of-home tea sales in COVID-ravaged India already exceed pre-pandemic totals. It is too soon to know what’s next, so focus on efficiencies in the here and now. The immediate priority is to recuperate and resume growth at a sustainable pace. Retailers that survive will see greater demand, better prices, and fewer competitors.

The path ahead is omnichannel. Elements include experiential online and face-to-face retail. Teach classes (online or in-person), start tea clubs, serve tea in the park. Offer carefully curated premium teas with an authentic (not necessarily artisan) back story and botanicals in sachets. Technology is underutilized by tea retailers. Accepting mobile orders and emphasizing takeaway (and drive-thru) communicates convenience and safety. Digital menus and QR codes that open to short videos showcase ambiance and preview the experience. Use predictive consumer intelligence to guide tea discovery online and to save on logistics expenses. Every specialty tea customer, young or old, is now a veteran online shopper seeking value (over price) and confronted with a dizzying number of choices. Concentrating on delivering tea delight – that transforming moment when uninitiated customers first taste premium quality tea – has never been more essential.

Adaptations by tea café and restaurant operators to meet new challenges including high turnover and more significant labor expenses are mainly defensive. Fewer footfalls in shopping districts, hospitality centers, and tourist locations and resorts are a formidable obstacle to full recovery.

While restaurants are experiencing aggressive consolidation and a rush of capital to finance M&A with more than a dozen IPOs in 2021, tea’s transformation will be mainly self-financed. There is little outside investment, and there are no IPOs or $650 million sales of home-grown tea chains to Starbucks on the horizon. Carve-outs are more likely than rollups. In 2021 Unilever shed 34 market-leading brands, including retail outlet T2, due to sluggish growth. The fact that CVC Capital Partners spent $5.1 billion, paying 14x EBITDA to acquire Unilever’s legacy brands, is notable.

Online sales show great promise, but garden-owned and direct-to-consumer brands are crowding a minimal marketplace for premium tea. Worse, automated comparison shopping suggests online prices will converge, driving down margins as advertising costs increase. Devising profitable business strategies, redesigning the retail experience, and remodeling storefronts will take time.

Innovations are emerging: Upscale boba tea rooms, nitro cold brew tea in bars, drive-thru iced tea shops, premium fruit tea outlets, subscriber-only tea clubs, and Livestream marketing. The mix of retail innovations and market-moving developments below (most visible in the West) will shape the future and fortunes of tea foodservice and foodservice suppliers in 2022.

Unprecedented Uncertainty

Defenses against pandemic-driven trends that appeared entrenched in 2020, including Lockdowns and the Pivot Online, continued to evolve in 2021. The restaurant segment and tea-themed cafés initially “hibernated,” as Samovar Tea Lounge founder Jesse Jacobs described. In the spring of 2020, he shuttered locations grossing $1 million annually, hopeful they would soon reopen. The office crowds in downtown San Francisco never returned. A year later, with depleted resources and no longer attracting outside investment, high-cost malls and downtown shops closed. By August 2021, well-respected operators like Roy Fong abandoned the Imperial Tea Room in Berkeley after 16 years. Shunan Teng, who founded Tea Drunk, closed her East Village tea shop in New York the same month. Mary Greengo, who founded Queen Mary’s Tearoom in Seattle in 1988, scaled back to a small packaged goods storefront across from the restaurant. In Sylvania, Ohio, Sweet Shalom Tearoom permanently closed after 20 years. Samovar Tea became an online-only tea retailer, and Jacobs now sells Detroit-style pizza at the former tea shops.

In contrast, small towns tenaciously supported Victorian-style tea rooms. Retirees sold many to a younger generation. According to Sinensis Research, there were more than 1,600 specialty tea shops in the US before the pandemic. Sinensis Research did not survive to count the survivors. Still, researcher Abraham Rowe would have found many fewer conventional “wall of tea” shops and far more bubble tea locations – 3,392 according to IBIS World.

In short, retail is reviving. Camellia Sinensis closed its Montreal tearoom in July 2020 and has been remodeled and will reopen in 2022. The LoKey Café in Spokane, Wash., opened this week, and in Atlanta, the Juniper Café opens next week.

Lockdowns

Always considered extreme, lockdowns for a time all but eliminated 20% of the tea industry’s revenue and continue to depress foodservice sales globally. Staff from chaiwallah stands in Mumbai to five-star restaurants on the Riviera shuttered their stores during the Alpha waves, shuddered in fear as Delta rampaged and now face nimble Omicron as the third year of the pandemic begins.

The National Restaurant Association estimated 110,000 US eating establishments closed in 2020, eliminating 2.5 million jobs as foodservice sales declined by $240 billion below estimates (off 24% year-over-year), making 2020 the worst year for restaurants in history – 2021 had to be better – and it was for a time. Vaccines built confidence, and at mid-year, the NRA forecast a 19% increase in foodservice sales to $789 billion. That didn’t happen. Summer lockdowns to control the Delta variant are to blame. While China, New Zealand, and Australia still tolerate zero-COVID periodic, geographically limited lockdowns like those currently in place to counter the Omicron variant are the new normal.

Diners will eagerly return whenever and wherever infections ease. Perilously-thin margins in the foodservice segment pose a more significant threat and will further tighten in 2022. On median, restaurants have only a 16-day buffer* (cash on hand) to meet their financial obligations.

Tea wholesalers servicing hotels, restaurants, cafes, and coffee shops were in disbelief in 2020 as standing orders simply stopped. Foodservice clients that survived often doubled their orders in 2021 to ensure stock in hand. Wholesalers weathered the crisis in part by supplying packaged tea blenders who worked overtime to restock grocery outlets with shelves stripped bare. The top sellers? Plant-based functional beverages with a reputation for health and wellness. In other words, tea. Sedate center-aisle tea overnight became the fastest moving of the fast-moving consumer goods in stores through much of 2020.

In 2021 the spotlight shifted to botanicals.

Botanicals

Plant-based, functional, botanical beverages (ignoring those with psychoactive properties) eroded tea sales the past two years. Still, there is no gloom for those whose first concern is customer well-being. Rishi Tea is now Rishi Tea & Botanicals with products on the shelf next to Bigelow Botanicals and Yogi Herbal Teas.

Consumers seek the calming promise of herbal teas during a time of anxiety and stress rather than traditional medicinal uses. The popularity of adaptogenic teas shows that evolving consumer taste preferences, healthy living habits, and convenience are the primary factors boosting sales.

According to Research and Markets the botanicals market globally was valued at $93.6 billion in 2020 and will achieve a CAGR of 6.63% from 2021-2026,

Brazil, Canada, the US, and a handful of European countries account for nearly the entirety of global growth in herbal tea because it is in these countries that the wellness trend that is boosting the category is strongest, according to market research firm Euromonitor.

Euromonitor writes that at 4% CAGR, “herbal tea represents most future tea growth in many regions. Usage is expanding beyond traditional medicinal and slimming to embrace a wide variety of new occasions resulting from modern wellness trends. This gives herbal tea a number of new areas to target in functional, indulgent, and hydration spaces.”

Europe consumes the largest share of botanicals globally. Germany has emerged as the leading market. Germans in 2020 consumed an additional two liters of tea to average 70 liters per capita, according to The German Tea & Herbal Tea Association. Most of that increase was from drinking botanicals.

Tea-only vendors are at a disadvantage competing with broader plant-based specialists such as Martin Bauer Group with a century of tea and botanicals expertise. In 2022 if you can’t beat them, join them; botanicals drive innovation, additional drinking occasions, and deliver health benefits. Relish the fact that virtually every botanical benefits with tea as its base.

As the pandemic ebbs, herbals will represent a much larger share of total consumption than in 2019, with calming and immune support functionalities showing especially high rates of interest, according to Euromonitor.

The average revenue created by tea per capita in the United States amounted to $32.53 in 2020. At the same time, per capita volume purchased by US consumers amounted to 400 grams. Per capita spending by Americans will further increase in the next few years, until reaching a per capita revenue of $46.95 in 2025.

– Statista Consumer Market Outlook

Tea Pivots Online

- Online sales are a lifeline for tea retailers large, and small. Statista market research estimates that 5.8% of total US revenue in the hot drinks market (coffee, cocoa, and tea) was generated through online sales in 2021.

- The US is a commodity tea market. The Beverage Marketing Corp., in 2018, estimated loose-leaf sales at 0.7% of the total US tea market, with ready-to-drink and tea bags accounting for 90% by value. About 23% of Americans drink tea daily compared to 27% in the US and 47% in the UK.

- Amazon and Walmart account for the greatest percentage of online tea sales in the US, but the more expensive and premium teas are offered on hundreds of websites that feature direct-from-origin loose leaf.

- Confined consumers who appreciate the convenience of doorstep delivery from their local tea shop’s selection of 100 teas soon discovered the more than 3,000 varieties globally. Delivery costs are reasonable, and niche vendors drive tea discovery by educating consumers about producers and specific origins.

- Producers that launched direct-to-consumer brands online, including Luxmi and Tata Tea 1868, broadened their base and earned far more per kilo than at auction. In 2021 every imaginable beverage competed online, forcing marketers to spend a fortune on advertising to generate incremental sales. The standout product is curated subscription boxes that deliver 75 to 1,000 grams of tea (enough for 15 to 45 cups) and sell for around $25 to $35 per month. Exclusive tea clubs that offer rare and premium teas charge subscribers $150 to $300 per year. Sri Lanka’s Dilmah Tea awards loyalty points to club members who earn discounts.

- Siliguri-based Teabox pioneered AI-powered curation that predicts seasonal and regional consumer demand for Indian tea. New Delhi-based Vahdam Tea expanded its capacity by partnering with Goodricke Tea to service a global market. In the US, Sips By, founded by Staci Brinkman, is an online subscription marketplace that delivers tea brands from around the globe.

- Brand marketers are experimenting with subscriptions, endorsements by tea bloggers, social media influencers, YouTube videos, Tik Tok, and live streaming.

- Quivr, a nitro-infused tea maker in Belchertown, Mass., promotes its $3.99 cans on Amazon Live(stream). Founder Ash Crawford told CNBC “It’s like clockwork or guaranteed that if we go live and I do a show, sales are increased for the next 24 hours by like 150%,” said Crawford.

- Art of Tea founder Steve Schwartz, in Los Angeles, is a master marketer and blender whose teas are featured on platforms including OzLink and The Collective.

- Zach Kornfeld is a novice in tea and one of the Try Guys an online influencer program with 7.3 million followers. In August 2020 he launched his Zadiko private label tea, selling 25,000 units valued at $500,000 in 12 hours.

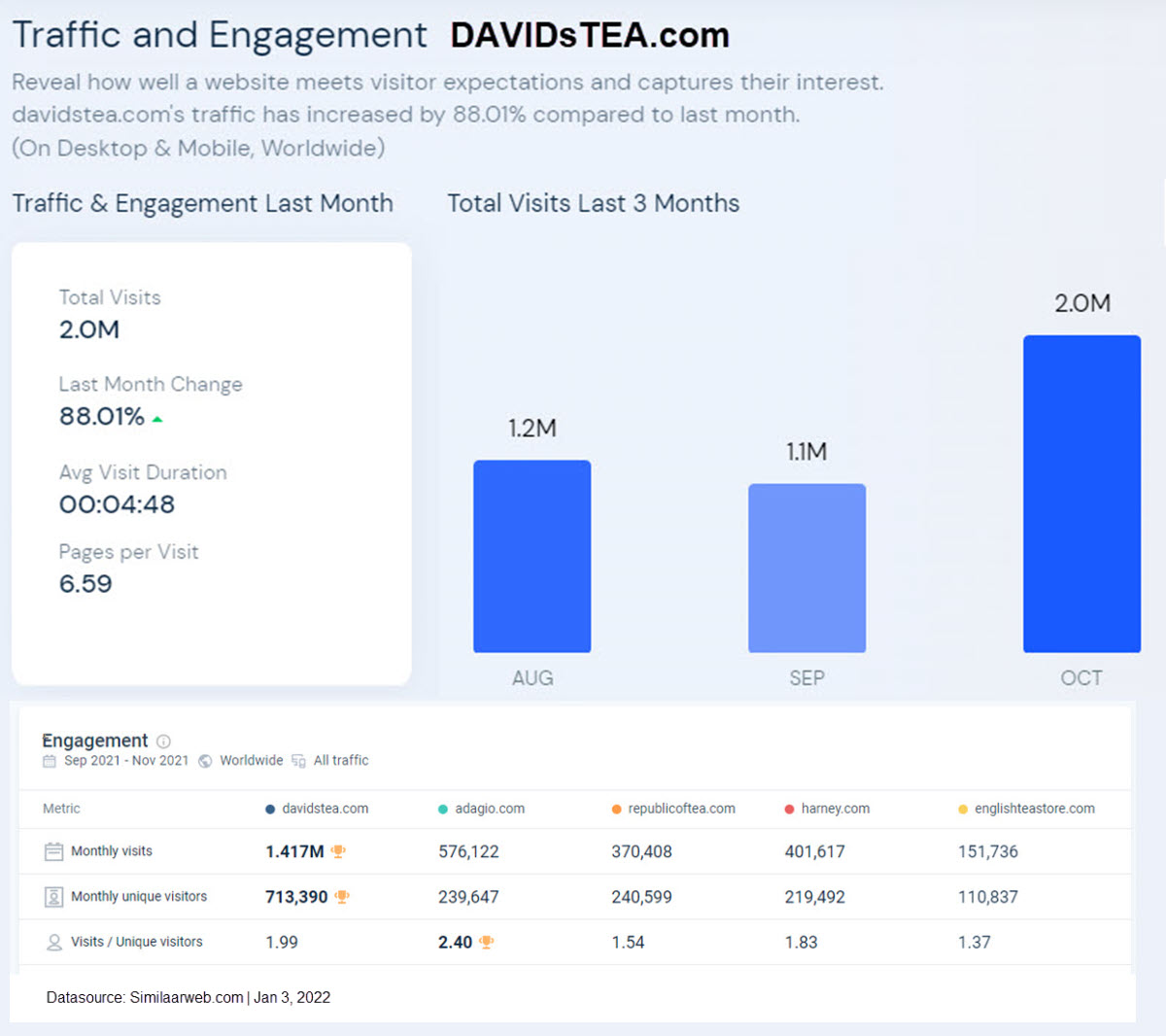

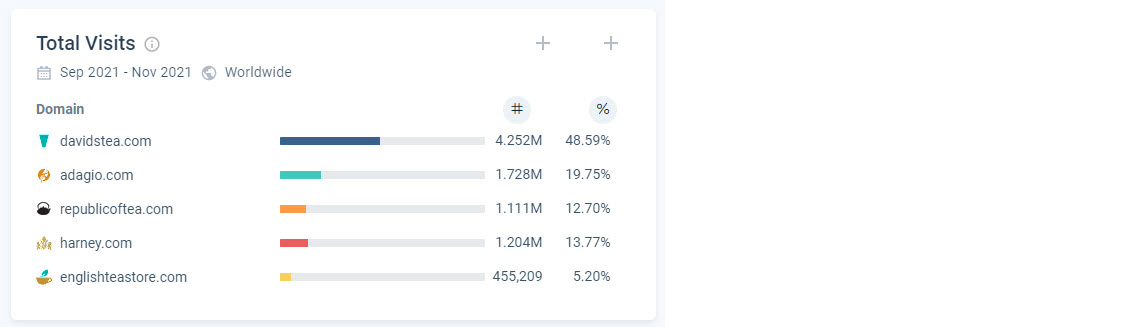

- Online sales resurrected bankrupt DAVIDsTEA, North America’s largest specialty tea chain. The company had fortuitously relaunched its website before March lockdowns forced the permanent closure of 166 locations including 42 US stores. In 2021 the company, trimmed to 18 locations, emerged from its financial peril as an online powerhouse and grocery brand with store-in-store pharmacy partner Rexall Drugs.

- The company earned $26 million as the pandemic raged in 3rdQTR20 with e-commerce and wholesale sales accounting for 84.3% of sales. The surge ended by 2021 but online sales remain impressive. The company is on track to earn $100 to $125 million in sales at 40% gross profit margins.

- “The 15.3% decrease in 3rdQTR21 sales year-over-year is largely due to a pandemic-fueled surge in online sales for our tea blends and accessories during the better part of fiscal 2020,” said Frank Zitella, President, Chief Financial and Operating Officer, DAVIDsTEA. “Progress achieved in transforming DAVIDsTEA can better be measured by the 18.5% sales increase compared to the second quarter, which is a better measure of our progress since we began our transformation into a digital-first tea merchant,” he said.

Coresight Research notes that the growth of single-channel online retailers, including marketplaces, now trails their omnichannel counterparts.

“The e-commerce boom should have been a heyday for digital-first retailers, yet one of the most striking features of this trend has been the general failure of online-only (or online-predominant) retailers to seize the opportunity to outperform in the only channel in which they compete,” writes Coresight CEO Deborah Weinswig. Stores serve as an online billboard for a retailer’s websites while online-only competitors are forced to pour money into advertising, she explains.

There were never enough local tea shops where US tea drinkers could taste a selection of good teas. There are many fewer now, making tea discovery online a top priority in 2022.

Bubble Tea

Sonic, Dunkin, and now Starbucks are blowing up the bubble tea trend following difficult days for the niche. Virtually all bubble tea is consumed away from home, and in 2020 just as lockdowns eased, a shortage of Taiwan boba virtually halted sales globally. The bubble tea market reached $2+ billion in 2019. Forecasts of $4.3 billion by 2027 are overly optimistic.

The category has momentum, with legendary fan support in Asia where bubble tea drinkers line up daily rain or shine.

Once a cheap 1980s Taiwan street-stall novelty made with hot powdered milk, boba (named for its tapioca pearls) is now served cold. The colorful beverage blurs the line between dessert and drinks, making it welcome at fast food and fast-casual restaurants, as well as cafes and kiosks. In 2015 vendors began enhancing ingredients, added fresh milk and cream, and customized orders by level of sweetness, adding whipped cheese, candied toppings, and fresh fruit.

Bubble tea has grown 76% on menus during the past four years, according to Datassential MenuTrends Infinite. It is the one tea beverage that benefited from the pandemic-induced growth in delivery.

“Bubble tea is loved most by Gen Z, a generation that’s grown up overall more used to the idea of global dishes and flavors,” writes Datassential. The sweet mix of milk and tea can be ordered at 20,000 US outlets, including major fast-food chains. IBIS World estimates 3,392 boba shops, including home-grown Kung Fu Tea, Lollicup, San Francisco-based Boba Guys, Gong Cha, Coco, ViVi Bubble Tea, Tiger Sugar, and Yi Fang Taiwan Fruit Tea.

Globally Taiwan bubble tea maker CoCo Fresh operates 3,000 locations. Gong Cha, also based in Taiwan, has more than 1,500 locations in 15 countries. China-based HeyTea, valued at $9 billion, operates 800 locations, and cross-town rival Nayuki which raised $656 million in its Hong Kong IPO to build 1,000 new storefronts, is valued at $2.5 billion.

In late December, a Tik Tok video revealed Starbucks had developed flavored “coffee popping pearls” for its cold-brewed “In the Dark” coffee. The company later confirmed that boba drinks are in trials in Palm Springs along with milk tea and Iced Chai Tea Latte at $5.25 for a grande.

Chai Point (Bengaluru, Karnataka)

Comfy chairs and inviting interiors to encourage leisurely conversation made Chai Point the ideal place to meet friends and take an office tea break with associates. Founded in 2010, the company had expanded to 169 locations during its first decade. Co-founder and CEO Amuleek Singh Bijral preserved the simple mission of “brightening lives and bringing people together” while building the venture into India’s largest chain of tea cafes with annual turnover of $25.5 million.

The company’s innovative online tools go well beyond standard sites and communications that focus on the customer contact point. Chai Point’s relationship-building through technology includes customer face recognition at point of sale, an extensive cloud computing infrastructure that connects to business customers for “touch-free” 30-minute ordering and delivery, a real-time inventory management system, and customer feedback apps.

Overnight COVID lockdowns cut revenue by $15 million. The pandemic transformed the company into a delivery dynamo operating from 120 locations and growing 120% in revenue as the first wave crested. Chai On Call delivery began in 2014. Chai Point launched vending services in 2016. During the crisis the company operated IoT vending machines at 4,000 locations. As locations closed Chai Point pivoted online, developing a packaged goods line of 15 instant teas sent directly to customers.

In March 2021 as the new wave crested, retail sales were close to 80% of pre-pandemic totals, vending had recovered by half with online retail steady Chai Point doubled down with 15 new products including multi-grain organic cookies and snacks.

Bijral told Fortune India, “We didn’t anticipate the second wave. People were cautious but the intensity of the wave and the kind of hysteria it created among consumers was sort of unexpected.” Like a cat, Chai Point once again landed on its feet.

“We ventured into vending, delivery and now, packaging, because we firmly believe that as a brand, we have to provide the customer an arms-length opportunity to pick our products. So, if the customer is at home, how will he get his tea? If he is in the office, he can go to the pantry and get a quick cup of chai. And if he is in the boardroom, he can get his chai served. When walking around, one can step into a neighborhood store and get chai,” Bijral told Fortune India.

Iced Tea Drive-thru (Amarillo, Texas)

Texans brag about their Texas tea, but on a blazing day in the oil fields, HTeaO, an iced tea drive-thru in Amarillo (West Texas), delivers another kind of liquid gold. The franchise chain, founded in 2009, has expanded rapidly despite the pandemic. “We’ve got thirty-two stores open, thirty-seven in some phase of construction, and another one hundred and fifty in development,” founder Justin Howe, President & CEO for HTeaO, told Texas Monthly.

HTeaO resembles a convenience stop with 26 fresh brewed sweet and unsweetened iced tea flavors that can be mixed, garnished, or blended with cut fruit. It’s a fun place to hang out with “happy hours” that draw crowds of patrons rewarded with loyalty points and complimentary tea. The focus is refreshment with pebble ice machines, Tik Tok-inspired recipes, and gallon jugs to go. Twelve-ounce cups are nowhere to be found in these shops. Start with 24 ounces, top off a 44-ounce cup with pineapple or cherries or choose the contractor’s favorite 51-ounce (1.5-liter) Peach-ginger or Sweet blueberry green iced tea. Buy a $3.50 tankard or pay $19.99 for four gallons to take away. Shelves are stocked with healthy snack options and a full line of YETI merchandise.

Construction workers arrive throughout the day to fill their on-site coolers with tea and fill five-gallon containers of double-pass reverse osmosis water, kids mix, and match at the self-serve fountain.

The above are just a few examples of experiential, tech friendly, customer obsessed retailers committed to the leaf we love.

Join me at World Tea Expo, for a presentation with additional examples of tea businesses “Coping with COVID” at 8 am Tuesday, March 22, 2022.

- Related

Tea Pivots Online

- *Cash buffer days are the number of days that a business can continue paying its typical outflows — such as payroll, purchasing supplier, or loan repayment — without bringing in any money, in the form of things like revenue, tax rebates, or transfers from investors’ or owners’ private savings.

Link to share this post with your colleagues

Signup and receive Tea Biz weekly in your inbox.

Never miss an episode

Subscribe wherever you enjoy podcasts: